What Are the Differences Between Buying and Renting a Property? A Simple Guide

Deciding whether to buy vs rent is a big decision. And it’s not an easy one.

Should you start buying a property and work toward homeownership? Or does renting a property make more sense for you right now? If you face any problem related iphone guide then visit this page.

Here’s the truth: there’s no perfect answer that works for everyone. We each have different personal circumstances and unique financial situations. What’s right for your friend might not be right for you.

But what can help is understanding the key differences between buying and renting a property. When you know how these options compare, you can make the choice that fits your life. And that’s what matters most.

Let’s look at the major differences between renting vs owning so you can decide with confidence.

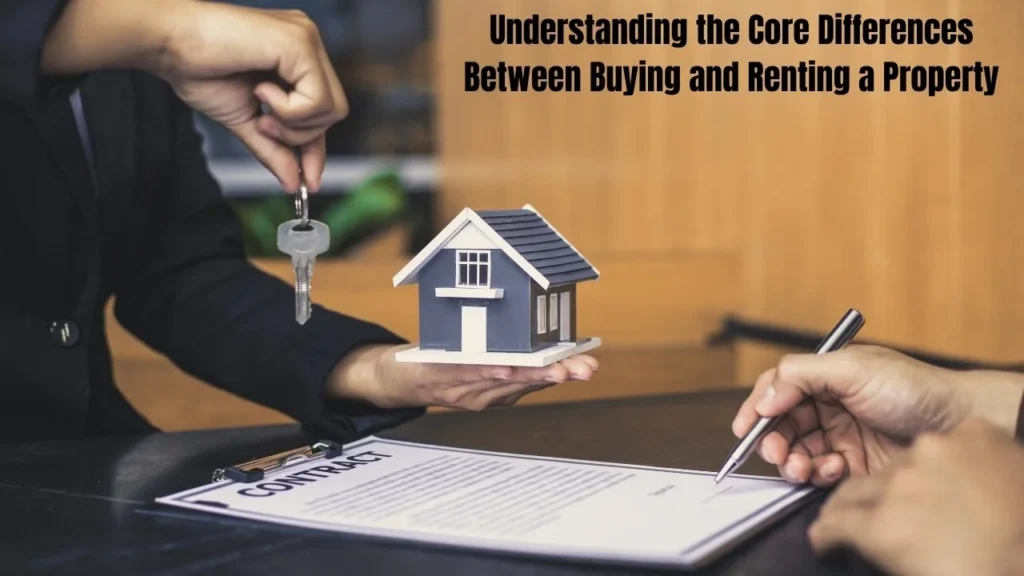

Understanding the Core Differences Between Buying and Renting a Property

Both buying a property and renting a property give you a place to live. But how they work? That’s where things get very different. If you have any issue related to Required in College then dont worry we also provide solution of this issue here on this website.

Where Does Your Money Go? Ownership vs. Monthly Payments

This is the biggest difference you need to understand.

When you’re renting a property, your rent payments go to your landlord each month. Your landlord owns the home, not you. You’re paying for the right to live there.

No matter how long you rent or how many monthly payments you make, you’ll never own the property. The property ownership stays with your landlord. And here’s something important: if you rent your whole life, you’ll still pay rent payments even after you retire. Those retirement housing costs never stop.

When you’re buying a property, things work differently. Your mortgage repayments go to your lender (like a bank or credit union). But with each payment, you’re building equity. You’re slowly buying the home. If you want to read about Bank Account than visit this page.

When your mortgage term ends (usually 15, 20, or 30 years), the home is yours. No more monthly payments. No more mortgage repayments. You own it completely.

“Rent payments disappear forever. Mortgage payments build ownership you keep.”

The flipside: Buying a property needs a big deposit upfront. Renting doesn’t require nearly as much money to start.

Monthly Payment Stability: What to Expect When Buying or Renting

Whether you choose to buy or rent, your monthly payments can change.

If you have a mortgage:

- A fixed-rate mortgage keeps your payments the same for years. You know exactly what you’ll pay.

- A variable-rate mortgage can change when interest rates rise or fall.

- Property taxes can increase each year.

- If you miss payments, you could face foreclosure. The financial consequences are serious.

If you’re renting:

- Your landlord can raise your rent, but there are rules.

- Most states require 30 to 60 days notice before a rent increase.

- Some cities have rent increase rules that limit how much landlords can charge.

- Annual rent increases are common in many areas.

The flipside: A fixed-rate mortgage gives you predictable payments for decades. But property taxes and maintenance can add unexpected costs that renters don’t face.

Maintenance and Repairs: A Major Difference Between Buying and Renting

Who pays when something breaks? This is another huge difference.

Who’s Responsible for Repairs?

As a homeowner, you pay for everything:

- Roof repairs can cost $5,000 to $15,000

- A new HVAC system runs $5,000 to $10,000

- Plumbing problems vary from $150 to $1,000 or more

- You need to budget for property repairs constantly

- Financial experts suggest saving 1% to 4% of your home’s value each year for maintenance costs

As a renter, your landlord handles it:

- Your landlord pays for major property repairs

- You just report the problem and they fix it

- Your landlord responsibilities are minimal

- You only pay if you caused the damage yourself

The flipside: Yes, homeowner responsibilities include expensive repairs. But you also have complete freedom to update and improve your home however you want.

Freedom to Customize: The Renovation Difference

When you own your home:

- Paint any color you like

- Knock down walls (with proper permits)

- Renovate the kitchen or bathroom

- Add features that increase property value

- You benefit from every home improvement

When you’re renting:

- You need landlord approval for changes

- Major renovations are usually not allowed

- You often can’t even paint without permission

- Any improvements benefit your landlord, not you

“Homeowners invest in their own future. Renters invest in their landlord’s future.”

The flipside: Customization costs money and time. Renters avoid this expense and hassle completely.

Lifestyle Flexibility: Mobility vs. Stability

Your lifestyle matters when choosing between buying and renting.

How Easy Is It to Move?

Renting offers flexibility:

- Give 30 to 60 days notice period (check your tenancy agreement)

- Easy to relocate for job opportunities

- Perfect for testing different neighborhoods

- Great for young professionals or military families

- No hassle of selling a property when you’re ready to move

Buying provides roots:

- Selling a property takes time (usually 2 to 3 months)

- You’ll pay real estate agent fees (typically 5% to 6%)

- Market conditions affect when you can sell

- A property chain can slow everything down

- Best if you plan to stay 5 years or more

Stability and Security: Control Over Your Housing Situation

Renting uncertainty:

- Your landlord can choose not to renew your lease

- If the property sells, you might have to move

- Rent increases can price you out of your home

- Less control over your long-term housing stability

- Risk of forced relocation at the owner’s decision

Homeownership security:

- You control when and if you move

- No landlord can ask you to leave

- Stable housing for your family

- Security of tenure as long as you make payments

- The home is yours to keep or pass to your children

The flipside: Homeownership ties you to one location. Renting lets you chase opportunities anywhere.

Building Wealth: The Long-Term Financial Difference

This is where buying vs renting really separates over time.

Equity Building vs. Zero Ownership

Buying builds wealth:

- Each mortgage repayment increases your ownership

- Homes typically appreciate 3% to 5% yearly

- You’re building an investment property for yourself

- Your equity becomes an asset you can borrow against

- You can leave the property to your family

Renting builds nothing:

- Rent payments are gone forever

- You gain zero equity

- No asset after years of payments

- You must build wealth through other investments

Important reality check: Real estate isn’t always the best investment. In expensive markets, renting and investing the difference might work better for the first 5 to 7 years. Every market is different.

Market Conditions: Is Now the Right Time to Buy or Rent?

Maybe you’ve decided you want to try buying a property. But then another question pops up: is now the right time?

Understanding Current US Housing Market Trends

The housing market changes constantly. Mortgage rates, home prices, and rental costs all shift based on economic conditions.

The central bank controls the base rate, which affects the cost of borrowing. When the base rate goes up to fight inflation, mortgage rates usually increase too. When rising interest rates make borrowing more expensive, some people step back from the property market.

But here’s what you need to know: even when interest rates rise, options still exist to help you get on the property ladder.

What Mortgage Options Are Available for Today’s Buyers?

First-time buyers have more choices than ever:

- FHA loans need just 3.5% down

- VA loans offer 0% down for veterans

- USDA loans provide 0% down for rural properties

- Conventional loans start at 3% down

- Longer mortgage terms make payments more affordable

- You can now find 30-year mortgage, 35-year mortgage, and even 40-year mortgage options

- Many states offer deposit assistance programs

Lenders are working hard to make homeownership accessible despite higher rates. The mortgage market keeps evolving to help buyers.

Incentives and Programs That Offset Higher Costs

Even with higher mortgage rates, help is available:

- Builder incentives like property discounts (sometimes 5% off)

- Homebuilder contributions toward your deposit

- Rate buydowns that lower your interest rates

- Green mortgages with better rates for energy-efficient homes

- Tax breaks for homes with good EPC ratings

Homes with an EPC A rating or EPC B rating mean lower energy costs. Your utility bills stay manageable, which helps offset other expenses.

Don’t let media headlines discourage you. When you look past the doom and gloom, real property options exist for people ready to buy.

Making Your Decision: Is Buying or Renting Right for You?

So how do you actually decide? Let’s break it down based on real situations.

When Renting Makes More Sense

Consider renting if:

- You’re planning to move within 3 to 5 years

- You don’t have savings for a deposit and emergency repairs

- Your career requires frequent relocation

- You’re in an expensive market where buying a property costs way more than renting

- You prefer predictable costs without surprise property repairs

- You value flexibility over building equity

- You’re still exploring where you want to settle

- You want to avoid maintenance costs and homeowner responsibilities

When Buying Is the Better Choice

Consider buying if:

- You’re planning to stay in the area 5 years or more

- You have stable income and employment

- You’ve saved for a deposit (even just 3% to 5%)

- You want to build equity and wealth

- You desire stability and control over your housing

- You want freedom to renovate and customize

- You’re ready for repair responsibility and maintenance costs

- You’re tired of paying someone else’s mortgage repayments

- You’re starting or growing a family

- You want predictable long-term housing plans

Questions to Ask Yourself Before Deciding

Financial questions:

- Can I afford a deposit without emptying my savings?

- Do I have 3 to 6 months emergency fund separate from my deposit?

- Can I handle a 20% to 30% increase in monthly payments beyond the mortgage?

- Is my job secure?

- What’s my debt-to-income ratio?

Lifestyle questions:

- Where do I see myself in 5 years? 10 years?

- Am I ready to handle property repairs?

- Do I want freedom to move easily?

- How important is customization to me?

- Do I value stability or flexibility more?

Market questions:

- What are homes selling for versus rent payments in my area?

- Are rents rising faster than home prices?

- What are current mortgage rates?

- Is it a buyer’s or seller’s market?

The Bottom Line: Understanding What’s Right for Your Situation

Don’t let anyone tell you there’s only one correct path. Don’t let media headlines about the property market scare you away from exploring your options.

If you’re serious about buying a property, look beyond the surface. Research the mortgage market. Talk to lenders about what programs exist for first-time buyers. Check out state programs for deposit assistance. Look into green mortgages if you care about sustainable housing.